# YT

**YT (Yield Token)** represents the right to the yield of staked interest-bearing tokens, and it's minted by staking **SY** and specifying a lock-up period.

### **Underlying Mechanism**

1. **Staking:** Users stake their underlying assets or yield-bearing assets, which are automatically converted into **SY** tokens.

2. **Minting:** After staking, **YT tokens** are minted by multiplying the staked quantity of SY tokens by the number of staking days. For example, staking 1 SY-wstETH and locking it for 365 days will mint 365 YT-wstETH. Therefore, **theoretically**, one YT token is anchored to the interest yield generated by one SY token per day.

3. **Redemption:** The interest income from SY will continuously accumulate in the corresponding **yield pool** over time. Users can choose to redeem the interest income corresponding to their YT tokens at any time. The redeemable value of each YT is calculated as follows:

### Important Considerations:

1. **YT has no expiration date** and is a generic ERC20 token**. Its redeemable value does not trend to zero over time, on the contrary, its initial value is 0 and it grows over time.** This differs from other protocols in the market.

2. To ensure the stability of UPT, the minted YT will be **non-transferable** (The current market demand for YT trading is low).

### **The Value Logic of YT**

YT is an **interest-rate-pegged token**. Theoretically, **1 YT is equivalent to the yield generated by 1 SY in one day.**

When YT is first minted, its **redeemable value** (i.e., the interest yield obtained by burning YT) **starts from zero and gradually increases over time**. Burning YT to redeem interest does not affect YT's redeemable value because the redeemed yield is proportional. **YT's redeemable value only decreases when new YT is minted**, but this decrease is temporary, as new interest will accumulate from the newly staked interest-bearing tokens, eventually compensating for this value.

Theoretically, the **anchor rate** corresponding to the redeemable value of YT stops growing when it reaches the actual interest rate of the interest-bearing asset. However, in practice, two scenarios may cause the anchor rate of YT to exceed this cap:

* **Early Burning of YT**: When some users burn their YT before the lock-up period of their staked interest-bearing tokens ends, the total circulating supply of YT decreases. Since the yield pool continues to accrue interest, this results in a relative increase in the interest redeemable per YT in the future.

* **Unredeemed Principal at Maturity**: If some users do not immediately redeem the principal of their interest-bearing tokens after the lock-up period expires, these unredeemed tokens continue to generate interest. This additional accumulated yield flows into the yield pool, further increasing the redeemable value per YT.

When this situation occurs, it leads to two outcomes:

* **Increased Returns for Long-Term Stakers:** In the future, burning YT will redeem more yield, increasing returns for long-term stakers. Simultaneously, the value of subsequently minted PT will decrease, **leading to a higher fixed rate for the corresponding SP**.

* **Arbitrage Opportunity to Lock In Higher Rates:** Users can, at what they perceive to be the highest interest rate point, stake more yield-bearing tokens to mint new YT and immediately burn them to capture interest yields, thereby **locking in a higher rate to avoid subsequent rate fluctuations**.

### **The mathematical model of YT**

While YT may appear simple on the surface, the ability for YT to be freely traded and for any YT holder to redeem yields at any time introduces a highly complex game-theoretic process and mathematical model.

The following, we construct a **minimal model** to calculate impermanent profit and losses.

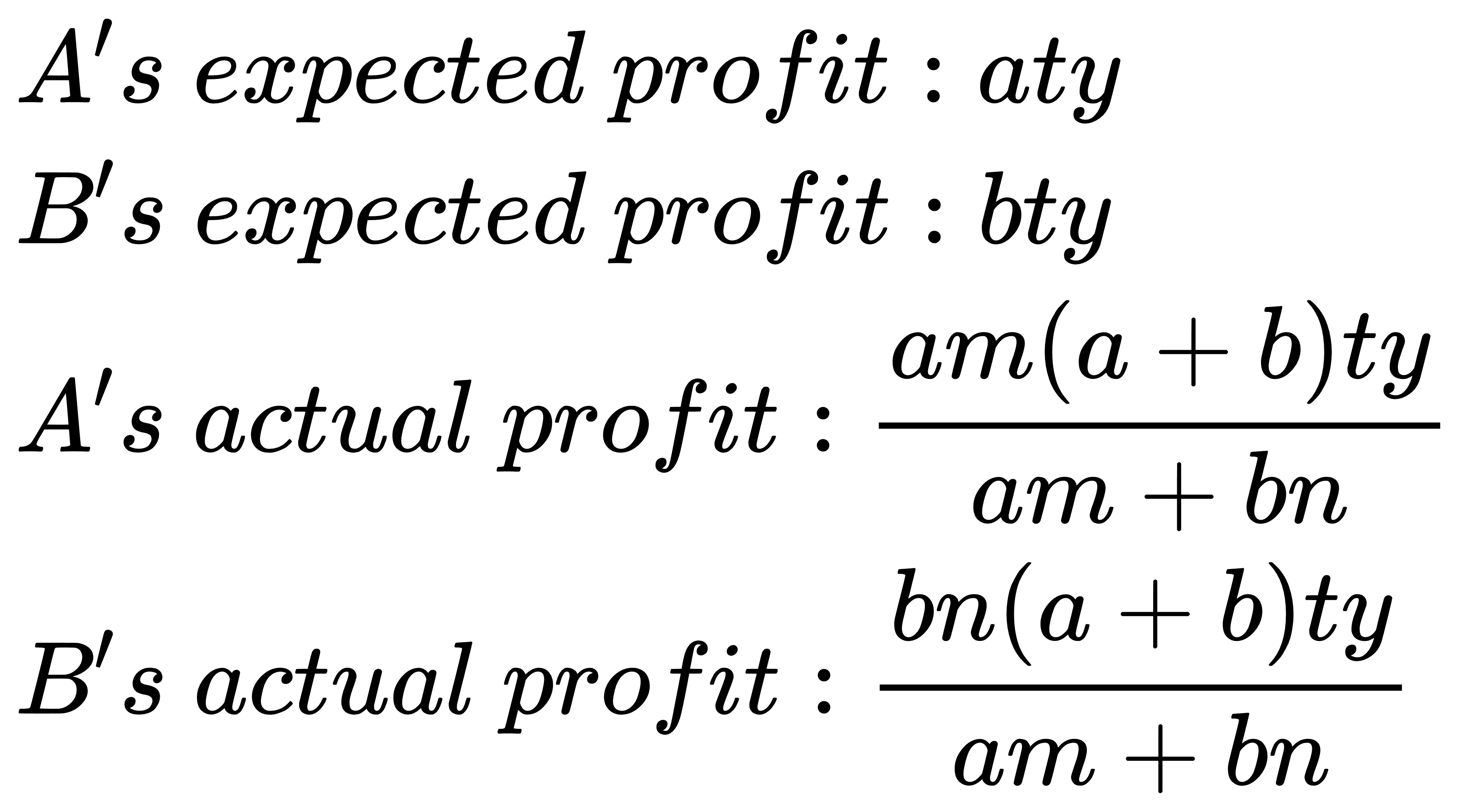

Assuming that the accumulated yields in the YieldPool is 0, and 1 YT is pegged to the yield produced by 1 yield-bearing token over 1 day, which we denote as **𝑦**.

User A stakes **𝑎** yield-bearing tokens and locks them for **𝑚** days, which will mint **𝑎𝑚** YTs. We will consider other users as a collective entity, referred to as User B, who stakes **𝑏** yield-bearing tokens and locks them for **𝑛** days, which will mint **𝑏𝑛** YTs.

After **𝑡** days:

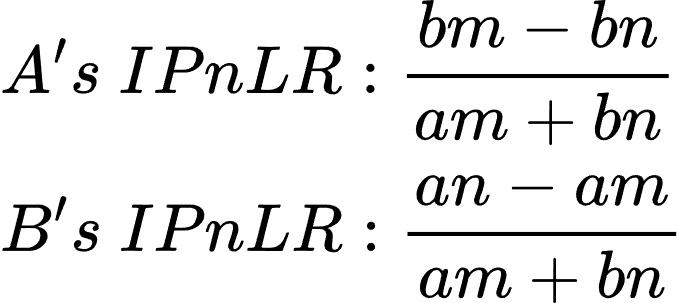

The **Impermanent Profit and Loss Ratio (*****IPnLR*****)** can be obtained by dividing the actual earnings by the expected earnings and then subtracting 1.\

\&#xNAN;***IPnLR = (Actual Earnings / Expected Earnings) - 1***

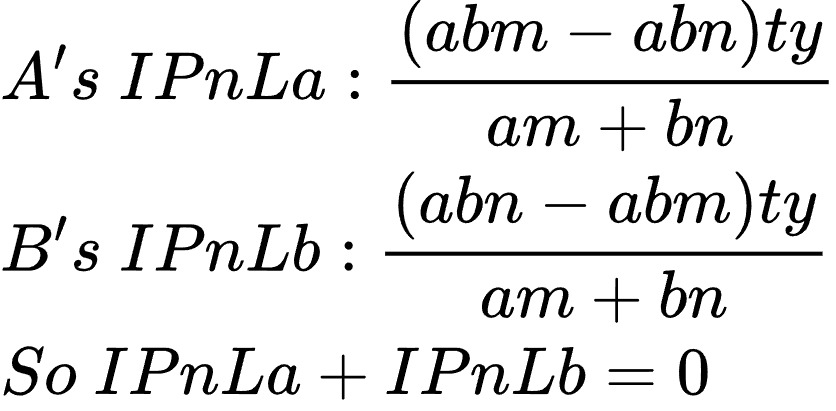

The **impermanent profit and loss (*****IPnL*****)** can be obtained by multiplying each user's **impermanent profit and loss ratio (*****IPnLR*****)** by their respective expected earnings.\

\&#xNAN;***IPnLa = IPnLRa \* Expected Profit\_A***\

\&#xNAN;***IPnLb = IPnLRb \* Expected Profit\_B***

From the above figure, we can deduce that there is an impermanent profit and loss conservation between User *A* and User *B*. If User *A* and User *B* lock up their assets for the same duration, both parties would experience no impermanent profit or loss. In other words, an individual user's impermanent profit and loss are correlated with the weighted average duration of other users in the staking pool.

Of course, the above is just a minimal model. The actual situation will be more complex due to the influence of multiple players in the game. Therefore, we will set a maximum lock-up time limit -- ***MaxLockInterval***. The closer the user's lock-up time is to ***MaxLockInterval***, the smaller the ***IL*** and the larger the ***IP***. Additionally, users can reduce ***IL*** and obtain more ***IP*** by redeeming their principal immediately upon the expiration of the lock-up period and then staking to mint REY again. When the user's lock-up time is ***MaxLockInterval***, there will definitely be no ***IL***.

Based on the model above, OutStake can help **long-term stakers earn greater returns**. We believe that staking inherently aims to make the underlying ecosystem more decentralized and secure. Therefore, users who protect the ecosystem over the long term should be rewarded more.

---

# Agent Instructions: Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter:

```

GET https://outrun.gitbook.io/doc/outstake/yield-tokenization/yt.md?ask=

```

The question should be specific, self-contained, and written in natural language.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.